USCB America is a collection agency based in Los Angeles, California that offers services in healthcare revenue cycle management. They were originally founded in 1915 as United States Credit Bureau, Inc. and have been in business for over 110 years.

They became 100% employee-owned through an Employee Stock Ownership Plan (ESOP) in 2003-2004. They have represented over 250 hospitals in 25 states and process over 19 million collection cases per year.

What is USCB America's History?

Despite their long history and industry accreditations, USCB America has a history of consumer complaints and legal actions against them. They paid a $2.75 million class action settlement in the case Brenda Jonsson v. USCB, Inc. for violating the Telephone Consumer Protection Act by making illegal robocalls. The settlement awarded at least $1.472 million to about 12,000 class action members.

Their profile on the Better Business Bureau website tells a different story. Though they have an A+ rating, they have had 92 complaints closed in the last three years, with an average customer review rating of 1 out of 5 stars on the Better Business Bureau.

The Consumer Financial Protection Bureau database contains approximately 180 complaints against the company. Common complaints against the company include attempting to collect debt that isn't owed, failing to provide adequate written notification of the debt, and using inappropriate communication tactics.

In describing her experience with the company, one reviewer on the BBB website wrote:

"I received an email from this company about a debt owed from a hospital bill 5+ years ago. When I called to try to resolve it I was told I had to pay them money so they could run my credit for $1.00 and otherwise they 'couldn't see' what I owed. They also tried telling me this is the only way they could 'save my credit.'"

Mistake #1: Panicking and Paying Immediately

Why Paying Right Away Hurts You

If you see USCB America listed on your credit report, your first instinct may be to pay whatever it takes to get the company to make the listing disappear. But before you do that, know that this reaction is exactly what the collection agency is counting on. These companies operate on thin profit margins, so they need a high success rate of collecting payments on debts in order to make a profit. They are hoping you will react out of fear and not strategy.

Critical fact: paying a collection account does not remove it from your credit report. Instead, the listing updates to "paid collection," potentially remaining on your report for up to seven years. You will have paid money for minimal improvement in your credit report and also validated a debt that may have errors or may not be collectable.

The Reality of Credit Reports

The chief damage of a USCB collection is to your credit score.

Collection accounts typically reduce credit scores by 100+ points, affecting mortgage eligibility, auto loans, credit cards, and employment opportunities. This will all still be true whether the collection account is listed as paid or unpaid.

If a debt collection agency is willing to settle a debt for 50% or less, that means they don't think the full debt is collectable. In fact, they may not think any of the debt is collectable. This should make you question their practices rather than rush to pay the debt immediately.

Mistake #2: Ignoring the Collection Entirely

How USCB Reports Without Notification

Many of the complaints against USCB America point to the company's practice of reporting debts to credit bureaus without notifying consumers directly. For example, one consumer wrote:

"I just got off the phone with USCB. I have apparently been in collections since November but received no phone call (they admitted they did have my number), no email (they also had this information), and no letter or anything in the mail (they had my address). I only found out today after applying to refinance my car, which I now cannot do because of the impact this has on my credit."

Another wrote:

"Just found out they have lowered my credit score by posting repeat and duplicate claims. I have never been contacted by these people and they have lowered my credit score by 22 points."

A third consumer reported the following experience with the company:

"One visit - 1 bill - 1 account number got 5 collections."

Ignoring a collection will not make it go away and leaving it on your report for an extended period of time can mean you are missing out on all sorts of financial opportunities in your life. Any loans you are able to take out will have higher interest rates, which will cost you thousands of dollars over the life of the loan.

Mistake #3: Trusting That the Debt is Accurate

Inaccuracies in the System

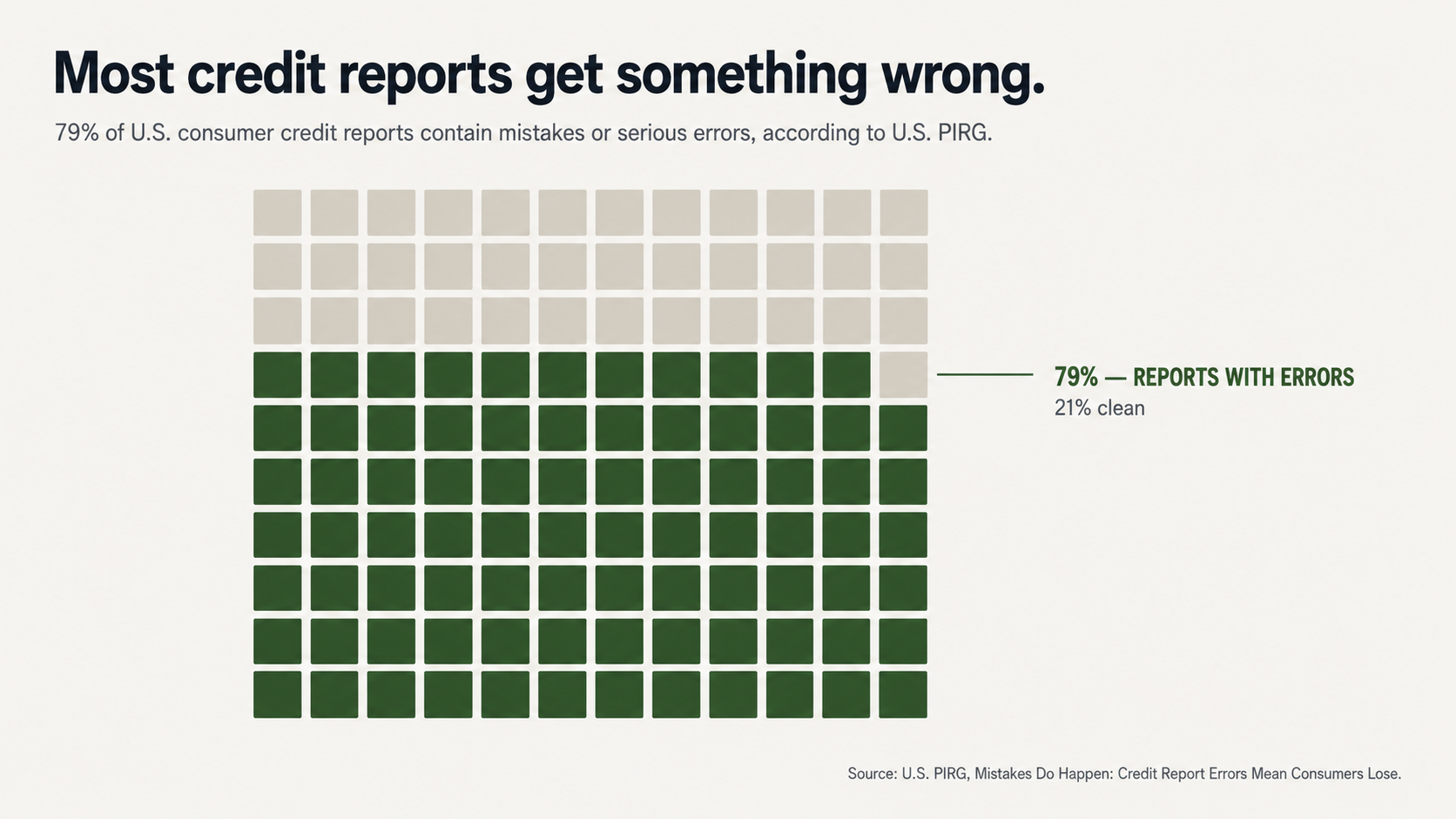

According to U.S. PIRG studies, 79% of credit reports contain mistakes or serious errors. That's not just a typo here and there. That means that almost 8 in 10 Americans have information on their credit report that is incorrect.

USCB America deals primarily with medical debt collection. Medical billing is rife with errors from denied insurance claims to incorrect patient identification to simple coding mistakes and transferred balances when patients are transferred between facilities. Several consumers have reported receiving collection notices for medical bills that were supposed to be covered by their insurance or showing a zero balance on their online healthcare provider account.

One reviewer on the Better Business Bureau website said:

"This company is a scam. They sent me invoices for unpaid bills from 4 years ago. We were completely covered by my husbands EXCELLENT insurance through his work. This company is a fraud."

Negotiated Settlements Reveal Inaccurate Balances

When a collection agency is willing to accept a negotiated settlement that is only a portion of the balance they are demanding from you, that should tell you that the balance they are demanding is not accurate. Debt collectors buy debt accounts from the original creditor for pennies on the dollar, so they have a lot of wiggle room in what they are willing to accept as a settlement.

If they accept a settlement that is 40% or 60% lower, that should tell you that the original balance is probably inflated or in question. Their willingness to accept a lower balance means that the balance they are demanding from you is not 100% accurate.

Mistake #4: Trying to Handle It Yourself

Information Imbalance

Debt collectors do this for a living. They know the laws and the loopholes and the buttons to push to get you to pay up. Most consumers only deal with a debt collection agency every once in a great while and do not have the same level of knowledge about the laws. This information imbalance works entirely in favor of the debt collection agency. They know how to use deadlines and threats to get you to pay up.

You do not have to talk to a debt collector on the phone. In fact, it is probably in your best interest to avoid it. Everything you say can be used against you, and you are unlikely to get useful information out of the representative on the phone.

Instead, request debt validation. The Fair Debt Collection Practices Act mandates validation when requested and prohibits collection attempts pending validation provision.

Several consumers have reported that USCB America routinely ignores requests for validation. For example, one consumer wrote:

"USCB began credit reporting me in June 2018. I called them and requested an itemized bill (not sent)... I again requested an itemized bill. The agent was very short with me and spoke over me several times. I have yet to receive an itemized bill."

If a debt collector cannot provide the validation you request, you may not actually owe the debt. If you work with a partner who knows how to request validation and use the absence of the requested documentation to dispute the debt, you can often get the listing removed from your credit report entirely.

Mistake #5: Assuming One Inaccuracy is a One-Off Issue

Recognizing a Pattern

If you find one inaccurate collection from USCB America on your credit report, that should tell you to suspect all of the information on your credit report. The same issues that caused one inaccurate listing to be placed on your credit report could cause others.

USCB America processes 19 million collection accounts per year. If they have systematic problems with their process, they will have systematic problems with their data. If you get one inaccurate listing removed, you should suspect every other listing on your credit report as well.

The Need for Systematic Review

Finding one removable listing should always encourage you to conduct a full review of your credit report for other potential problems. The same problems that caused one removable listing to appear could cause others, both from the same collection agency and from others. You may be able to remove additional listings from your credit report that you did not find on your own.

Professional credit repair specialists will review your full credit report as a matter of course. They will know what to look for and what to request and how to document it in a way that helps you the most. In conducting a systematic review, they may be able to find additional removable listings that you did not find on your own.

Conclusion

USCB America has been around for over a century, but that does not mean all of their practices are accurate or fair. The $2.75 million settlement, 92 BBB complaints (three years), approximately 180 CFPB complaints, repeated reporting without notification documentation, and validation request ignoring warrant careful consideration.

The five mistakes consumers commonly make when dealing with USCB America collections all stem from perfectly understandable motivations: the desire to make a problem go away as quickly as possible, the belief that an official-looking letter must be legitimate, and the idea that you can handle it yourself as a practical solution. But in all of these cases, acting on these motivations can end up hurting you in the long run.

What to Do Next?

If you have a listing from USCB America on your credit report, do not panic and do not pay it immediately. Instead, the listing could have errors or not have the correct documentation and may not be a legitimate listing at all. In some cases, it may be possible to remove listings from USCB America entirely from your credit report.

At FightCollections.com, we specialize in fighting debt collectors and helping consumers remove questionable collection accounts from their credit reports. We know about the documentation issues and reporting violations and validation issues that plague companies like USCB America.

Contact us today for a free consultation. Instead of allowing an aggressive debt collector to push you around, why not let a professional work for you? Your credit score plays a role in almost every major financial decision you will make in your life. Do not leave it to chance.