Does Zwicker and Associates have a collection account on your credit report? Before you take action or pay them anything, you should understand exactly who is demanding your money and if they even have the right to collect the debt from you.

Zwicker and Associates, P.C. is a debt collection law firm based in Massachusetts that was founded in 1981. Instead of a typical debt collection agency, this company employs attorneys in 48 states who are primarily tasked with suing consumers and using aggressive legal tactics on behalf of their clients.

What is their reputation like?

As of January 2025, Zwicker and Associates has 684 complaints filed with the Consumer Financial Protection Bureau. They have also been defendants in 567 cases in federal court, according to PACER.

In addition, federal courts have found the company to be in violation of the Fair Debt Collection Practices Act on more than one occasion.

In 2005, a federal court in New York ruled as a matter of law that Zwicker and Associates’ collection letters violated the FDCPA because they failed to clearly state the name of the creditor and contained confusing language. (Sparkman v. Zwicker, E.D.N.Y. 2005)

Four years later, another federal court in New York found the company in violation of the FDCPA for failure to clearly state the amount of the debt. (Weiss v. Zwicker, E.D.N.Y. 2009)

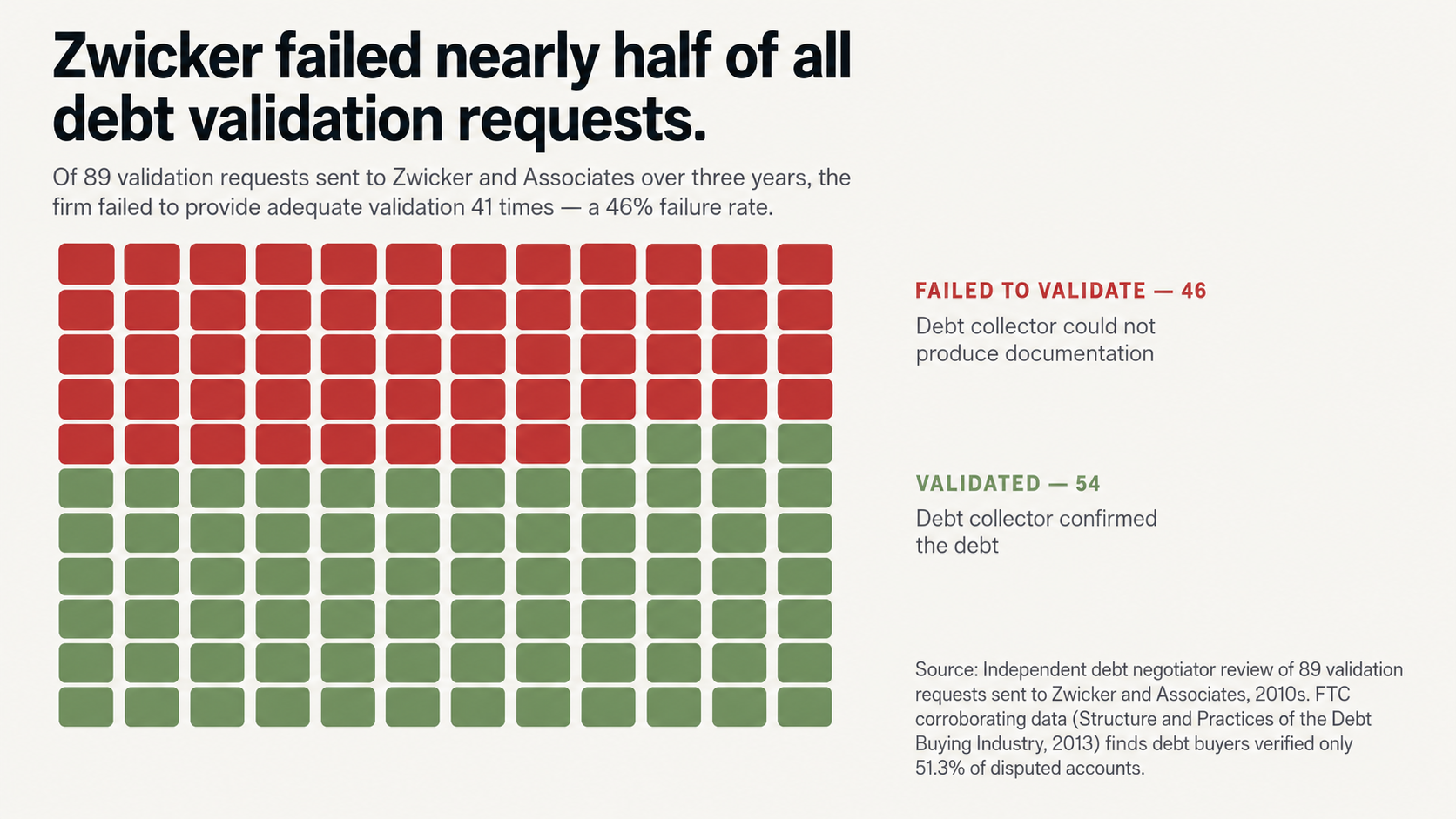

But perhaps the most telling indicator of the company’s reputation is the fact that one debt negotiator reported sending 89 debt validation requests to Zwicker over the course of three years and found that the company failed to provide adequate validation 41 times. That’s a 46% failure rate.

Is the debt from Zwicker and Associates legitimate?

How common are collection errors?

Are you certain that the debt that Zwicker and Associates claims you owe actually belongs to you?

According to a study by U.S. PIRG, 79% of credit reports contain errors or other major mistakes. This means that the odds of your credit report containing an inaccuracy are actually higher than you might think.

In the debt collection industry, accounts are often sold, transferred, and resold. With each change in ownership, the documentation and records for the account can get lost, the account numbers can get transposed, and debts can get attributed to the wrong person altogether.

Zwicker and Associates represents a variety of major creditors and debt buyers, including American Express, Discover, Chase, LVNV Funding, and CACH, LLC. This means that the debt the company claims you owe may have changed hands several times before it was placed with Zwicker.

In 2013, the Federal Trade Commission found that nearly half of all disputed debts couldn’t be verified by debt collectors. This is consistent with the 46% debt validation failure rate we discussed earlier. If nearly half of all disputed debts can’t be verified, then the real question isn’t “do errors happen?” but rather “how many people are paying debts they don’t owe?”

What kinds of documentation problems are we talking about?

You might be surprised to learn that Zwicker and Associates was connected to one of the largest process serving scandals in recent history.

The company used a process serving business called American Legal Process, which was shut down for engaging in systematic “sewer service.” This is a practice where process servers file false affidavits claiming that defendants were served with legal papers when, in fact, they were not.

The scandal ultimately resulted in a petition to the state to vacate about 100,000 judgments that were entered based on the company’s illegal serving practices.

In at least two documented cases (Discover Bank v. Nieves and Discover Bank v. L.N.), judgments of $10,241 and $9,000 respectively were vacated by Queens Civil Court after Zwicker and Associates was unable to provide proof that the defendant had been properly served.

If judgments in verified court cases were thrown out because Zwicker and Associates couldn’t provide the documentation to prove that the defendant had been served, then why on earth would you trust that the documentation for the debt they claim you owe is any more reliable?

Should you pay what Zwicker and Associates claims you owe?

What happens when you pay a collection?

Many people assume that if they pay a collection account, it will be completely removed from their credit report. Unfortunately, this is not true.

When you pay a collection account, the account’s status will be updated to show that it’s been paid, but the negative account will still remain on your credit report for up to seven years from the original delinquency date.

Additionally, paying a collection account can even restart the statute of limitations in some states, and it may be considered an admission that you owe the debt.

If the debt was reported in error — or if it doesn’t belong to you at all, or if it’s already past the statute of limitations — then paying it can actually make your situation worse instead of better.

The debt collection industry makes money by relying on consumers to react emotionally and urgently instead of strategically. Zwicker and Associates operates on a tight deadline, with some original creditors reportedly requiring the company to file a lawsuit within 90 days of placement.

This is all designed to get you to act before you think.

What are your rights before paying?

Under federal law, you have the right to request verification of a debt before you pay a single dollar.

Using the Fair Debt Collection Practices Act, you can require a debt collector to provide you with documentation that proves the debt, including:

The exact amount of the debt

The name of the original creditor

The date of the last payment

Documentation to show that the debt belongs to you

Requesting debt validation isn’t just a good defense — it’s a good offense, too. In many cases, it can help expose a debt collector who doesn’t have the documentation to support their claims.

As we mentioned earlier, every time a debt is sold, transferred, or resold, the risk of lost or incomplete documentation increases. If you demand verification, there’s a good chance that the collector may not be able to provide it.

In light of Zwicker and Associates’ 46% debt validation failure rate, demanding verification isn’t just your right — it’s a necessity.

What if Zwicker and Associates threatens to sue you?

How likely are they to file a lawsuit?

In CFPB complaint narratives, consumers have reported that Zwicker and Associates told them they were going to be sued, that they would have their homes taken away, that their wages would be garnished, and that their accounts would be seized.

One consumer even reported that they were told to sell their belongings and clear out their bank account so they could pay the debt immediately. These are all classic tactics designed to get you to react emotionally instead of logically.

The reality is that it costs money to file a lawsuit. Before they decide whether or not to sue you, a debt collector will typically perform a cost-benefit analysis to determine whether or not you and your debt are worth the investment.

In most cases, the balance on your debt isn’t worth the attorney fees, court costs, and time it takes to pursue you through the legal system.

Of course, that isn’t to say that Zwicker and Associates never files lawsuits. They do, and because they’re a litigation-heavy debt collection law firm, they file far more lawsuits than the typical debt collection agency.

However, if you understand that their threats of a lawsuit are often just a tactic instead of a certainty, you’ll be in a much better position to respond rationally instead of emotionally.

What are consumers saying about their experience with Zwicker and Associates?

Despite having an A+ rating with the Better Business Bureau, Zwicker and Associates has an average customer review rating of just 1.38 out of 5 stars.

The reason for the discrepancy is that the BBB rating is based on how well a company responds to complaints, not how satisfied consumers are with the company’s service.

Here’s what one BBB reviewer wrote in September 2023:

“My bank account was levied because someone in their office flagged my account as a no contact. Why would I tell you to not contact me if I agreed to a previous repayment schedule and only had 1 payment left? Everyone associated with the law office and contact center are rude and lack empathy.”

Another consumer filed a complaint with the CFPB, stating:

“They constantly send people to my ex-wife’s house or call my number or my ex-wife’s house threatening with wage garnishment or collections. I have had numerous conversations with them to stop harassing my kids and my ex-wife but the harassment continues.”

Can you get the collection removed from your credit report?

What has to happen for removal?

In some situations, you may be able to have a collection account removed from your credit report altogether.

If the information that the debt collector reported is not accurate, you can dispute the account and have it deleted. If the debt is fraudulent or the result of identity theft, you can have it removed. And if the debt collector can’t verify the debt within a reasonable amount of time as required by law, the credit reporting agencies have to delete the listing.

Ultimately, the question is whether or not the information that Zwicker and Associates has provided to the credit reporting agencies will stand up to scrutiny.

Given that federal courts have found the company’s collection letters violated disclosure requirements — and given the company’s 46% debt validation failure rate — you may have a very good case for questioning the accuracy of the information that’s appearing on your credit report.

Instead of paying first and asking questions later, it’s usually a better idea to dispute first and then pay later. This preserves your options and puts the burden where it belongs — on the debt collector to prove their case.

Why does it make a difference if you have professional representation?

When you have a credit repair professional involved in your case, everything changes. Debt collection agencies know that when you have professional representation, you’re far more likely to know your rights and assert them.

You’re more likely to file a complaint when a debt collector violates your rights. And you’re more likely to file a lawsuit if necessary to protect your rights.

When debt collectors know that you have professional representation, they’re less likely to push their luck. They’re less likely to be aggressive. And they’re more likely to try to come to a reasonable agreement with you.

There’s another benefit to having professional representation, too — the emotional factor. Dealing with debt collectors can be incredibly stressful, and companies like Zwicker and Associates know how to use that stress to their advantage.

When you have a professional representing you, you don’t have to deal with the stress at all. You don’t have to field threatening phone calls. You don’t have to try to decipher confusing letters. And you don’t have to make decisions under pressure.

What should you do next?

Why is there a time sensitivity?

Zwicker and Associates operates on a very tight timeline. Industry insiders say that some of the company’s original creditors require them to file a lawsuit within just 90 days of receiving a new account.

This means that the window for you to take action is limited, and the longer you wait, the more likely it is that you’ll be facing a lawsuit before you’ve even had time to figure out your options.

Zwicker and Associates is a huge company, with 21 offices throughout the country and about 686 employees. They bring in an estimated $192-$250 million per year in revenue. This isn’t a small-time operation that’s just going to forget about you if you ignore their letters and phone calls.

However, the same sense of urgency that Zwicker and Associates uses as a weapon can also be a powerful tool in your hands if you know how to channel it into the proper dispute procedures.

By acting quickly and strategically instead of emotionally and reactively, you can be in control of your own outcome instead of letting the debt collector dictate your next moves.

How can FightCollections.com help you?

If Zwicker and Associates is on your credit report, you know what your questions are. Is this debt legit? Can they prove it? And what are my options before I pay them a single dollar or accept their claims at face value?

At FightCollections.com, we specialize in challenging collection accounts through the proper dispute procedures.

We know all about the documentation problems, the regulatory violations, and the verification failures that plague debt collection agencies like Zwicker and Associates. We know how to demand proof of a debt, and we know how to respond when the proof doesn’t come.

Don’t let a debt collection law firm bully you into making decisions that could damage your financial future. Don’t pay them money for a debt you may not even owe just because some stranger on the phone told you to. And don’t try to navigate this complex situation by yourself when you have professional advocates who are ready to help.

Contact us at FightCollections.com today for a free consultation.

Let us review your situation and assess your options. Let us help you develop a strategic plan for dealing with the Zwicker and Associates account that’s on your credit report. The questions you need answers to are too important to leave to chance.